by Maria151 | Jul 26, 2025 | Automobile

Buying auto insurance in Nashville isn’t just about finding the cheapest policy—it’s about making sure you have the right protection for Tennessee’s unique driving conditions and legal requirements. From busy city streets to unpredictable weather, the right policy can save you from serious financial stress.

Here’s what every driver in Tennessee should know before getting or renewing their policy.

Tennessee is a fault-based state, which means the driver who causes an accident is financially responsible for the damages. To drive legally, you must carry at least:

-

$25,000 bodily injury liability per person

-

$50,000 bodily injury liability per accident

-

$15,000 property damage liability

This basic coverage keeps you legal, but it won’t always cover the full costs of a serious accident, especially with today’s expensive medical care and car repairs. Many Nashville drivers choose higher limits to avoid paying out of pocket if the damages exceed the minimum requirements.

Do You Need More Than the Minimum?

While the state’s minimum coverage helps you stay compliant, it may not protect you enough. Here’s why you might want more:

-

Medical expenses can easily exceed $25,000 in a serious accident.

-

Property damage for newer or luxury vehicles can be much higher than $15,000.

-

Minimum liability won’t pay for your own car repairs if you’re at fault.

Adding collision and comprehensive coverage can protect your car against accidents, theft, vandalism, and even weather-related damage—important for Nashville’s sudden storms and icy winter roads.

When I compared Nashville car insurance, I noticed many companies offer affordable packages that go beyond the bare minimum without dramatically increasing your premium.

Factors That Affect Your Nashville Car Insurance Rates

Several things influence how much you’ll pay for coverage in Nashville:

-

Your driving record – Tickets and accidents can raise your premium.

-

Where you live – Downtown areas with more traffic and theft risk often have higher rates.

-

Your vehicle type – Newer, more expensive cars cost more to insure.

-

Annual mileage – Driving fewer miles could qualify you for a low-mileage discount.

-

Credit history – In Tennessee, insurers may use credit-based insurance scores to determine risk.

Knowing how these factors work can help you take steps to lower your premium over time.

Tips to Save on Nashville Auto Insurance

You don’t have to sacrifice good coverage to save money. Here are a few ways to cut costs:

-

Compare quotes from multiple insurers before renewing.

-

Bundle your policies with renters or homeowners insurance for extra discounts.

-

Maintain a clean driving record to avoid surcharges.

-

Ask about discounts for safe driving, good students, or anti-theft devices.

-

Review your coverage regularly to make sure it still fits your needs.

Even small changes can make a big difference in your premium.

Final Thoughts

Before buying or renewing your policy, take time to understand Tennessee’s requirements, your coverage options, and how different insurers calculate rates. Minimum insurance might be cheaper upfront, but it could leave you paying a lot more later.

It’s always worth comparing Nashville policies that give you solid protection at an affordable price so you can drive with peace of mind.

by Maria151 | Jul 18, 2025 | Automobile

Car insurance is a necessary expense, but that doesn’t mean you have to overpay. In a busy city like Louisville, where traffic congestion and higher risk factors can raise premiums, finding the best deal takes a little effort.

The good news? With the right approach, you can uncover hidden savings and lower your monthly costs without cutting back on essential coverage. This ultimate checklist will help you navigate the process step by step.

Compare Multiple Quotes from Different Insurers

Never settle for the first quote you receive. Each insurance company uses its own unique formula to calculate premiums, which means the same driver could get very different rates from different providers.

By comparing at least three to five quotes, you’ll gain a better idea of what a fair price should be for your situation. Online tools make it easy to see rates side by side, so you can choose a plan that balances cost and coverage.

This is one of the most effective ways to find cheap car insurance in Louisville Kentucky and ensure you’re not missing out on a better deal elsewhere.

Take Advantage of All Available Discounts

Most drivers qualify for multiple discounts but don’t always know to ask for them. Here are some common savings opportunities you should look for:

-

Safe driver discounts for maintaining a clean record.

-

Low-mileage discounts if you drive fewer miles than average each year.

-

Bundling discounts when you combine auto with home or renters’ insurance.

-

Good student discounts for teens or college drivers with high grades.

-

Telematics-based savings for signing up for usage-based programs.

Always ask insurers about available discounts—you might be surprised at how much you can save with simple changes.

Choose the Right Type of Coverage

Not every car needs full coverage. If you drive an older vehicle with a lower market value, liability-only insurance might make more sense. This can significantly lower your premium while still keeping you compliant with Kentucky’s minimum insurance requirements.

On the other hand, if your car is newer or you still have a loan, maintaining comprehensive and collision coverage is essential. The key is striking the right balance between protection and affordability.

Consider Adjusting Your Deductible

Your deductible is the amount you pay out of pocket before your insurance kicks in. By choosing a higher deductible, you can reduce your monthly premium. Just make sure you’re comfortable with the amount you’d have to pay if you file a claim.

This strategy works especially well for drivers with a good safety record who rarely file claims.

Drive a Vehicle That’s Cheaper to Insure

Some cars cost more to insure simply because they’re expensive to repair or have higher theft rates. If you’re shopping for a vehicle, look for models with strong safety ratings, lower repair costs, and built-in anti-theft features. These factors can make a noticeable difference in your insurance premiums.

Maintain a Strong Credit Score

In Kentucky, insurers can use your credit-based insurance score when calculating your rate. A better credit score often leads to lower premiums because it signals financial responsibility.

Paying bills on time, reducing debt, and monitoring your credit report for errors can all help improve your score over time, which can translate into cheaper car insurance.

Final Thoughts

Finding affordable coverage in a busy city like Louisville doesn’t have to be complicated. By comparing quotes, asking about discounts, adjusting your deductible, and making smart vehicle choices, you can bring your premiums down without losing valuable protection.

Most importantly, review your policy every year to make sure it still fits your needs and budget. Rates change, new discounts become available, and your driving habits may evolve—staying proactive is the best way to keep saving.

by Maria151 | Jul 10, 2025 | Others

When most Pittsburgh drivers think about what influences their car insurance premiums, they often point to age, driving history, or the type of car they drive. But there’s one crucial factor many overlook—credit score. In Pennsylvania, including Pittsburgh, your credit score can play a surprisingly large role in how much you pay for auto insurance.

If you’ve been wondering about the credit score impact on car insurance PA, this post breaks it down—how it works, why insurers use it, and what Pittsburgh residents can do about it.

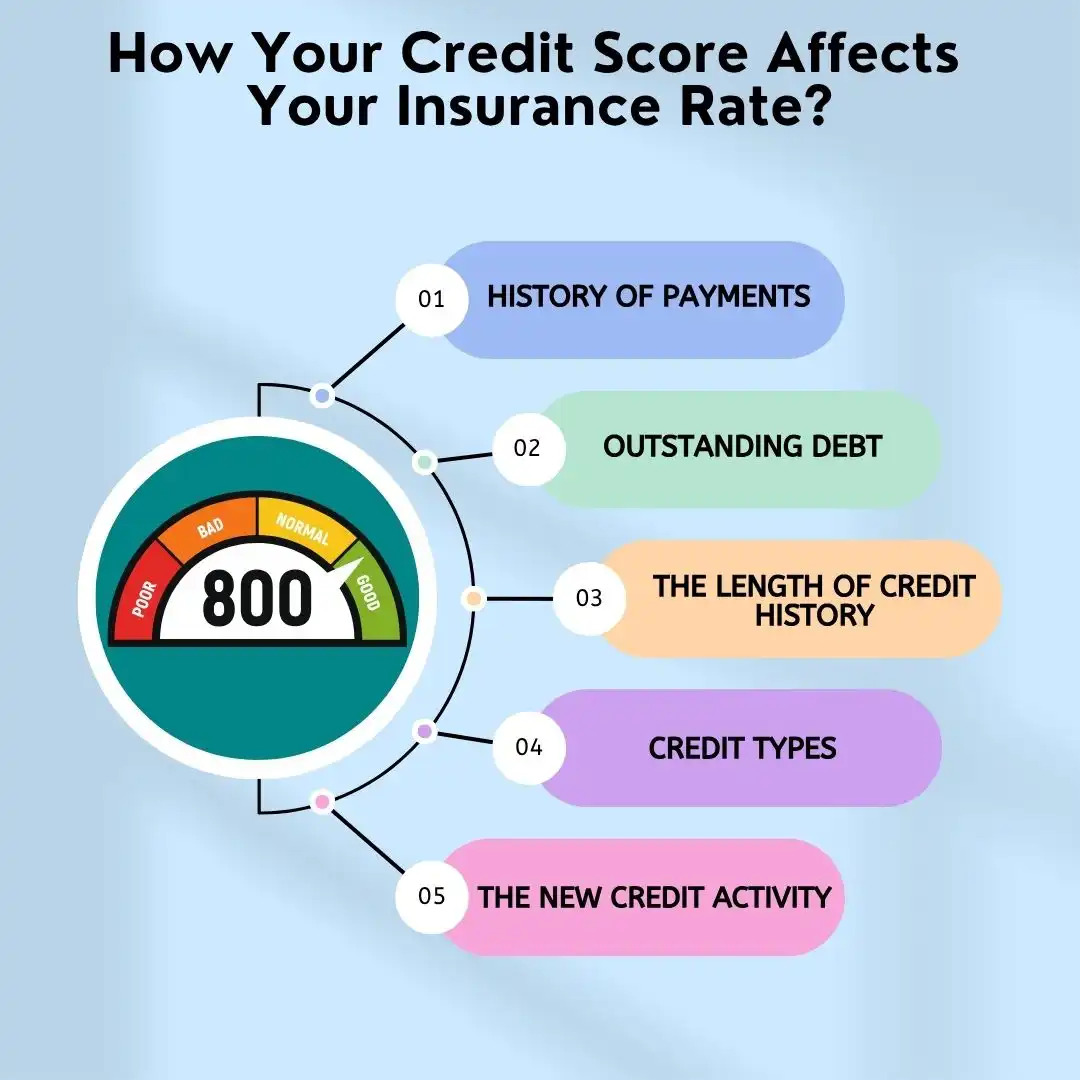

Why Do Insurers Use Credit Scores?

Insurance companies in Pennsylvania are allowed to use your credit-based insurance score to help determine your auto insurance premium. This isn’t your full credit score (like FICO), but a modified version that includes:

-

Payment history

-

Outstanding debt

-

Credit inquiries

-

Length of credit history

-

Types of credit used

Statistically, studies show that people with lower credit scores tend to file more claims. Whether that’s due to financial stress, higher-risk behavior, or simply correlation—not causation—it still influences how much you pay.

The Credit Factor in Pittsburgh Rates

In a city like Pittsburgh, where rates already fluctuate based on neighborhood, traffic congestion, and weather-related claims, your credit score adds another layer of pricing. For example:

-

A driver with excellent credit (750+) in Squirrel Hill might pay $1,350/year.

-

The same driver with poor credit (under 600) in the same ZIP code could pay over $2,000/year—even with no tickets or accidents.

This is why credit score is often considered a “hidden” premium factor. You could be a safe driver and still be penalized for financial missteps from years ago.

How Big Is the Difference?

According to industry data:

-

Drivers with poor credit in Pennsylvania can pay up to 60–70% more for car insurance than those with good credit.

-

In Pittsburgh specifically, the average cost difference ranges between $500 to $800 annually depending on the insurer and ZIP code.

That makes credit score impact on car insurance PA one of the most financially significant factors—especially in urban areas like Pittsburgh where base rates are already higher than the state average.

Which Insurers Penalize Bad Credit the Most?

Some companies weigh credit scores more heavily than others. Based on 2025 market trends:

-

GEICO and Progressive tend to be more forgiving with poor credit.

-

Nationwide and State Farm apply moderate penalties.

-

Smaller regional providers, including Erie Insurance, may place less emphasis on credit and more on driving history.

Always compare multiple quotes to see which insurer treats your profile most fairly. Shopping around is key, especially if your credit isn’t perfect.

How to Improve Your Insurance Rate Through Credit

If your premium is higher than expected, your credit score could be the reason. Here’s how to improve it—and your insurance rate along with it:

-

Pay bills on time – Payment history makes up a major portion of your insurance score.

-

Reduce credit utilization – Keep balances low on credit cards and loans.

-

Avoid opening unnecessary new accounts – Too many inquiries can hurt your score.

-

Check your credit report – Look for errors that could be dragging your score down.

-

Request a policy review – Once your score improves, ask your insurer to re-evaluate your premium.

For more context, you can read this Wikipedia article on credit-based insurance scores to see how they’re used nationally.

Final Thoughts

Yes—your credit score absolutely affects car insurance premiums in Pittsburgh. And while you can’t change your neighborhood or local traffic patterns, your credit score is one factor that’s largely within your control.

If you’re shopping for new coverage or feel like you’re overpaying, explore how much influence your credit may be having. And when comparing policies, make sure to consider the credit score impact on car insurance PA—it could save you hundreds per year.